Compound interest is sort of like taking your vitamins. You don’t really see the benefits right away but in the long run, it’s doing all kinds of wondrous things like making you stronger (financially, in the case of interest) and full of life (hello, extra funds to travel with come the golden years).

(Need a place to stash your travel funds? Automate your savings inside the nav.it money app.)

Ready to get your vitamin CI (compound interest)?

Get rich(ish) quick

Compound interest is interest-on-interest. For example if you have $100, and the interest rate is 5 percent per month, you would earn $5 in interest and a total of $105 in your account. In the next month, you would earn 5 percent on the $105 for a new total of $110.25, and so on and so forth, earning interest on the new balance each month.

This accelerates your earnings over time as the interest-on-interest grows.

There are two things that affect the rate at which you earn compound interest: time and interest rate. The longer you can invest for and the higher the interest rate you earn, the more benefits you will reap from compound interest.

Start investing yesterday

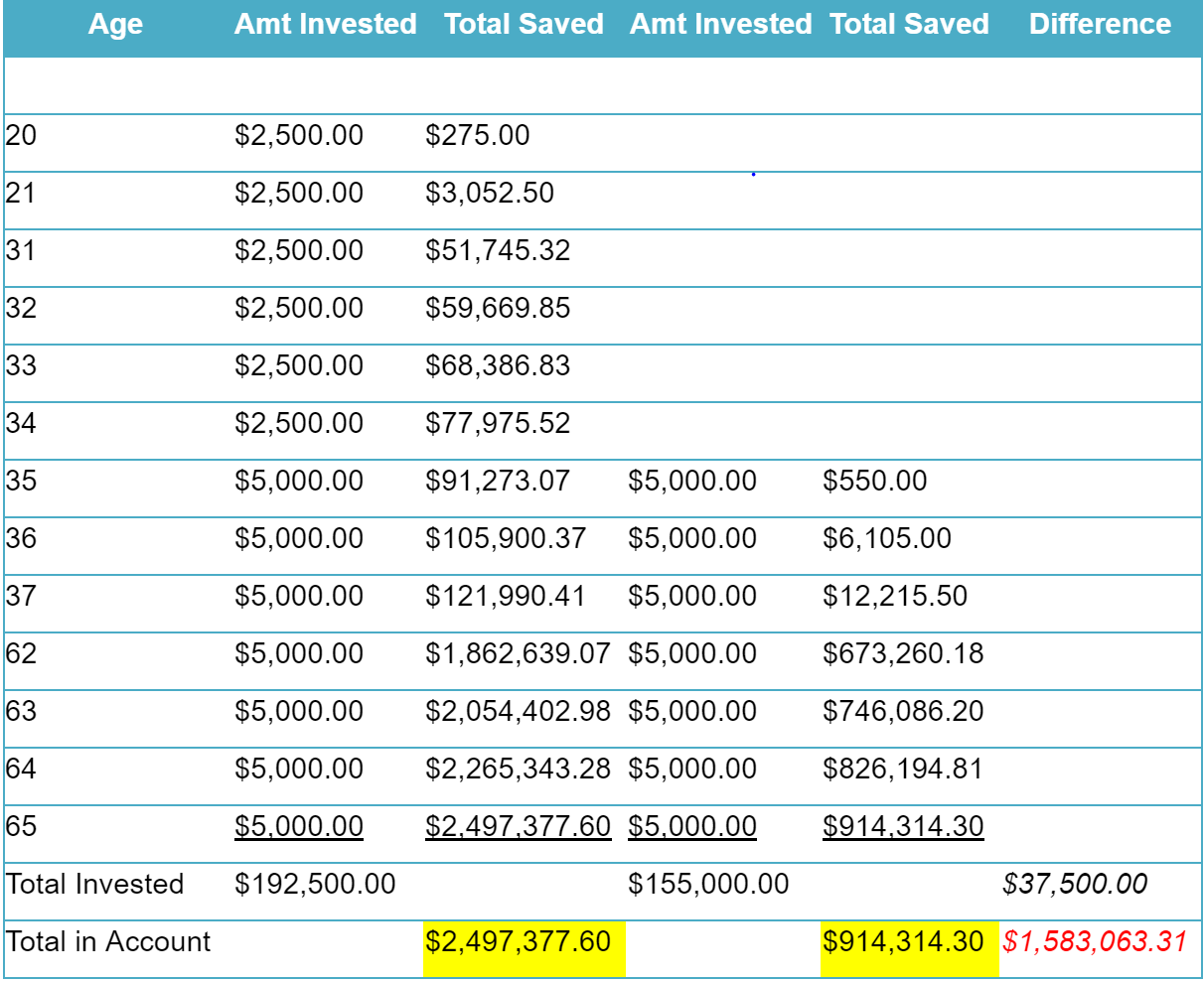

The sooner you invest, the sooner you reap the benefits of compound interest, and the longer too. Take a look at this example. Two people are investing: one starts at 20, and the other at 35. Notice the difference in total saved by the time of retirement is huge.

The highlighted values show the totals you will have in your account assuming a 10 percent compounding interest rate. Check out how much higher it is than the total you invested (that’s free money).

More importantly, check out how much of a difference there is between the Suzy saver who started putting away funds when she was 20 versus the average person who starts saving when they are about 35 (that’s probably when good sense kicks in and we stop putting so much money toward Friday night ragers).

The difference in actual investment is only $37,500 but the compounded effect is over $1.5 million…that’s magical. But it’s also very real. Start saving now.

When compound interest bites us…

It’s great to get compound interest in the form of savings but compound interest isn’t so great when we have to pay it. You’ll notice that if you don’t pay your credit card bills for a month, you’ll have to pay interest. And the next month you don’t pay, you’ll pay interest on your total plus the previous month’s interest as well. That’s the negative effect of compound interest (womp womp).

Retirement is a long way away for most of us, and saving for it might seem like something you can put off until you find your first few gray hairs. But you’ll be missing out on the huge benefits of compound interest. Invest early, even if you can’t invest a lot right now.

We’re trying to change the narrative around money but change can’t happen with a one-sided conversation. That’s why we’re excited to bring different voices and experts to share their wisdom. Send us an email and let us know what you think. And remember the nav.it money app offers you free tools for checking in and managing your money moves. You can download it at Google Play and the Apple Store.